Now that the kids are back at school, the roads and trains are full and Australia has kicked back into full capacity, it’s time to peer into our crystal ball again.

Unlike President Trump, I am happy to admit I’m borrowing a famous quote from the hugely popular series ‘Game of Thrones’. But what is the connection to financial markets I hear you say? Just as in the television series, it is a warning of bad things to come and if you continue to say it for long enough you will eventually be proven right.

Many market commentators, including ourselves have warned that we are in the last stages of the economic expansion that started way back in 2009. While we can confidently say that we are in the last stage, it is difficult to predict when it will finish and what the catalyst will be that triggers the next recession. We do know however that as the economic cycle ages, market volatility increases, interest rates will likely rise and corporate earnings will slow – factors that the last quarter of 2019 brought us in spades.

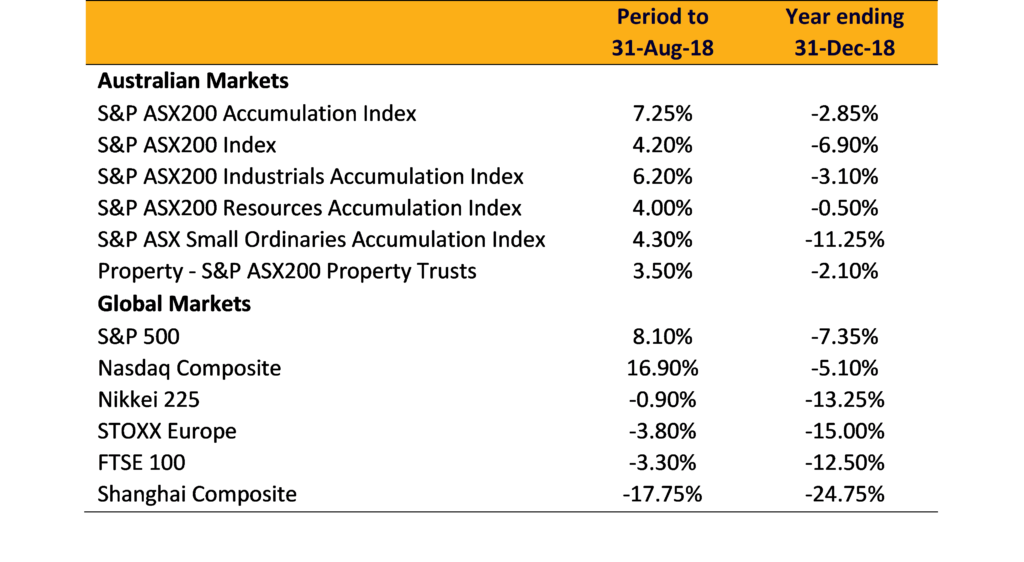

Market concerns about slowing global growth and the US/China trade war generated substantial falls in equity markets from August through December 2018, so much so, that what had been looking like respectable returns turned negative as outlined in the table below.

What’s the outlook from here for our financial markets?

Although we believe we are in the last stages of economic expansion, it is not all doom and gloom despite our warning that ‘winter is coming’.

The falls noted in the table above show just how quickly market sentiment can change and how large the impacts can be upon portfolio returns. Since these falls however, markets have once again started to rally on hopes a compromise will be achieved in the US/China trade war and a halt in the interest rate increases in the USA. These market swings are symptomatic of the increasing volatility that we have been warning of.

It is well known that US President Trump loves to tweet and, in the early days of his Presidency, he aligned his performance with the strength of the US equity markets. With so much turmoil surrounding his Presidency he will no doubt be looking for opportunities to once again claim any market strength as his own making.

The ‘Trump Effect” on financial markets

President Trump certainly can influence markets. Should he announce that a trade deal has been struck with China and some tariffs abolished, we believe markets could rally strongly, heading back to previous highs.

Given his perceived loss over the US government shut down and ongoing Robert Mueller enquiries Trump could do with some good news. Due to that political cost, we think a trade deal is the more likely short-term outcome.

The continued lack of inflation (we still believe it will rise albeit at a slower pace) and the prospect that the US Federal Reserve is on hold for at least the next six to twelve months, markets certainly have the environment to climb higher, they simply need a catalyst. Over to you Mr Trump!

Caution should be taken for long-term outcomes for financial markets

Despite the opportunity for a bounce in equity markets we remain cautious on the longer-term outcomes.

Should the markets regain the highs of last year we will once again recommend profits be taken where valuations are stretched. At the end of the day, we remain in the last quarter of the cycle and bar the onset of recession, global central banks will continue to shrink their bloated balance sheets despite the hold in interest rate increases.

As central banks reduce their balance sheets, it decreases the amount of liquidity in the system. Liquidity is the lifeblood of markets and the sheer quantum of liquidity we have seen these past ten years has been a large driver of the significant positive returns.

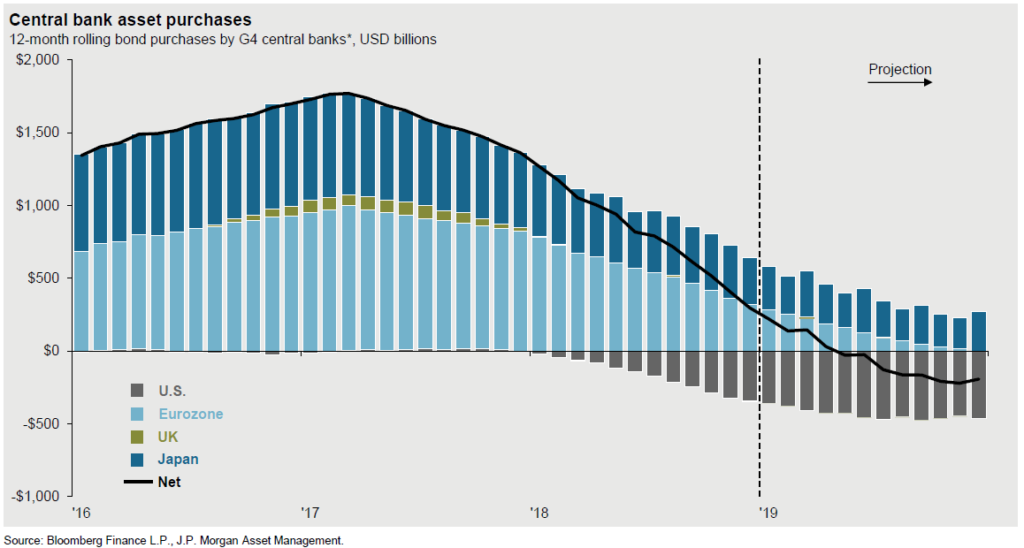

Central bank asset purchase programs to turn negative

As outlined in chart above from J.P. Morgan, we have never been in a situation where this amount of liquidity has been withdrawn, so we are in uncharted waters.

If we have a gradual reduction, as expected, markets can still post solid positive returns, however, given the liquidity reduction, we expect those returns to be lower than what we have witnessed in recent years.

Interest rates should remain steady for the next 12 months

Since 2015, the US Federal reserve has lifted its cash rate eight times from a low of 0.25% to the current rate of 2.5%, while the European Central Bank and the Bank of Japan retain negative interest rates and our own Reserve Bank of Australia remains on hold at 1.5%.

Regardless of the interest rate environment, the directional movements of interest rates are what we are most interested in. As central banks increase rates they remove liquidity from the banking system, a similar outcome to the one highlighted above.

The current economic slowdown means that most central banks are likely to keep rates at current levels for the next six to twelve months, however, that may quickly change should the drag of a trade war evaporate and inflation starts moving higher.

There have been numerous discussions as to whether inflation will ever spike again and while we won’t bore you with a detailed recap, the quick summary is that ageing demographics and productivity gains from robotics and artificial intelligence mean the inflation genie is well and truly back in its bottle.

For those who have been through a few economic cycles, you know it is dangerous to assume things are changed forever.

US inflation expected to creep higher

Although we have had to revise how quickly US inflation will grow, our view remains that US inflation will creep higher from here. This view is based on tariffs being inflationary; settlement of the trade war will take away a growth drag, and that wages in the US are rising once again.

US unemployment hit a 49 year low of 3.7% in November 2018 and there were 6.8 million job openings and only 6.1 million people seeking employment. This level of tightness in the labour market has to push wages higher.

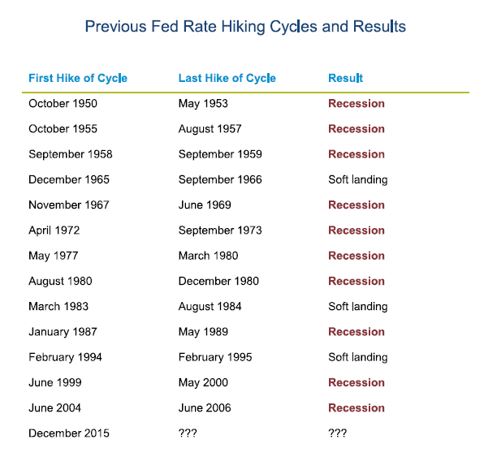

As the following table from Bloomberg, Mauldin Economics highlights, we have only had three occasions out of the last thirteen rate hiking cycles where we have not landed in a recession.

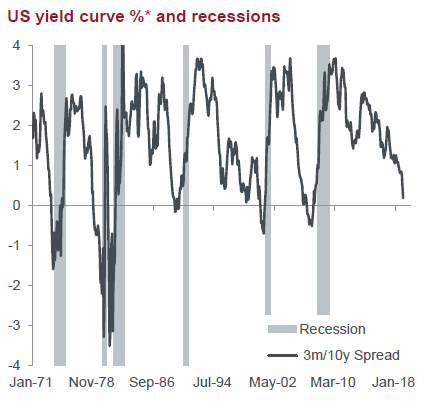

The reason that we remain cautious is that market cycles tend to end and recessions are triggered by either interest rate increases or excesses in markets as shown in the chart below (courtesy of Janus Henderson – Economic and market charts January 2019).

Excesses in markets

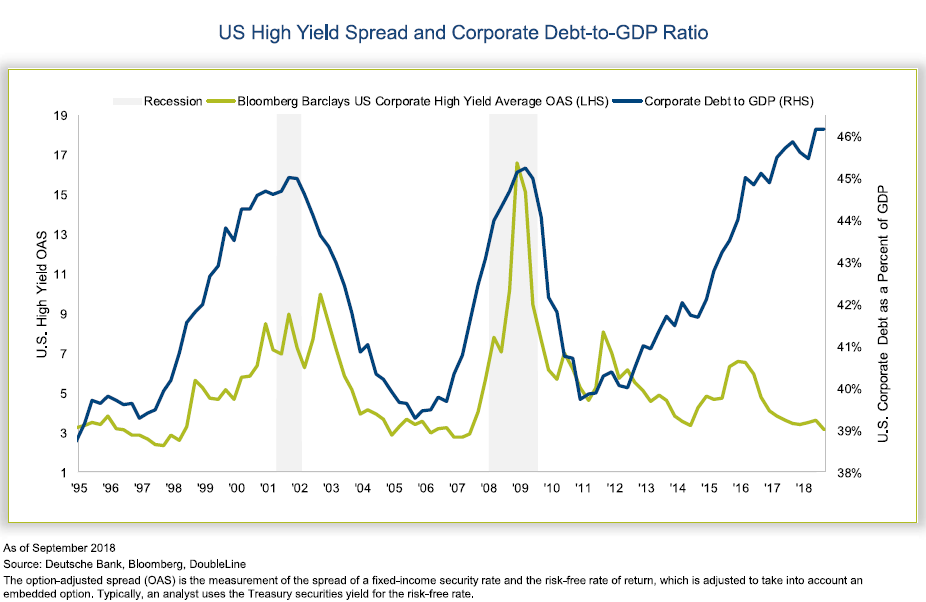

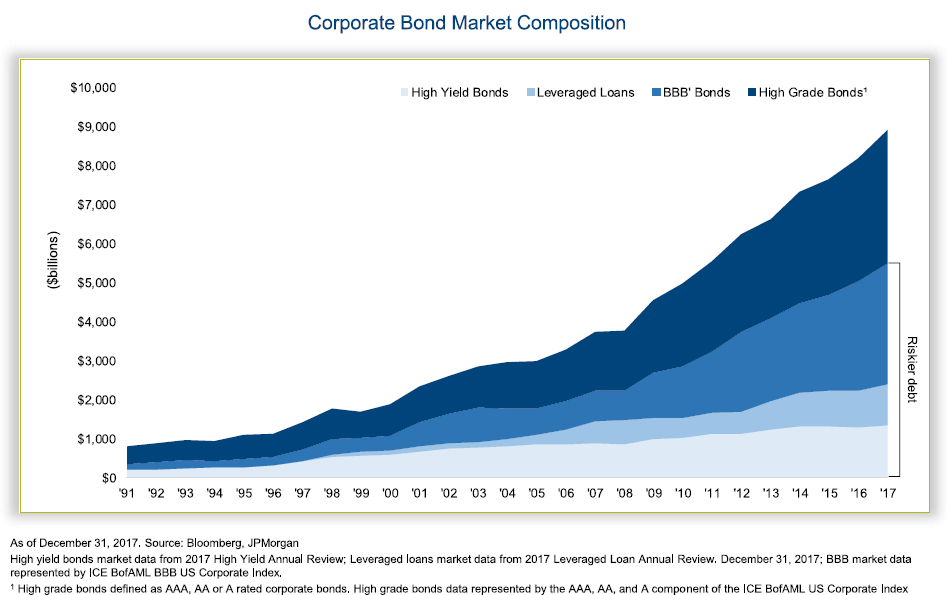

One area of excess that we are currently monitoring is the build-up in corporate debt. Thanks to the incredibly low interest rate environment and strong earnings growth, ever increasing numbers of corporates have capitalised on investor demand for higher yielding investments.

The chart below outlines how the corporate debt to GDP ratio has reached new highs, surpassing levels attained prior to the previous two recessions.

Of significant concern is the fact that the yield on offer has been declining while the outright level of debt increases. In other words, as companies take on more debt and become riskier, the rate that investors have been receiving as compensation has decreased.

Giving further cause for concern is that the biggest growth in debt has occurred in BBB rated bonds, this is just one notch above junk bond status.

A small increase in interest rates could see large numbers of these companies struggling to repay these bonds. Some will argue that this is not a concern as interest rates will stay low for a very long period, however, if global growth does continue to slow and corporate earnings fall, it will not take long for investors to reprice these risky assets downwards.

While this is mostly a US phenomenon, it still has ramifications for Australian investors. If default levels or interest rates increase in the US, those Australian companies that borrow overseas (predominantly our banks) will also face higher interest rates.

There should be no doubt that the banks will look to pass this increased cost onto borrowers, at a time when Australian consumers are already becoming more cautious due to little wage growth and a retreating housing market.

Portfolio implications for investors

This update might paint a gloomy image of the future and the natural response would be to move all assets into cash, however, a knee jerk reaction is not necessarily needed.

The reason that this update is somewhat gloomier is that we see a lot of potential risks that could derail markets. As we are likely in the final stages of the market cycle, the phase is characterised by increased volatility. However, this does not mean that there will not be opportunities to generate reasonable returns.

As we move through this late stage of the cycle it is paramount that additional care is taken in portfolio holdings. We are past the time to blindly follow indexes higher, we are now at a stage where active management should shine. They key will be to act as and when opportunities present themselves.

In order to be in that position investors need to walk a fine line between capital preservation and generating a sufficient return.

As we have noted above, we think returns from here will be harder to eke out but that does not mean we should throw caution to the wind and chase those exotic investments offering the ‘potential’ of high returns.

A well-diversified portfolio of high quality assets will help to weather any approaching storm.

Andrew Aylward is Chief Investment Officer at Keep Wealth Partners.

Keep Wealth Partners Pty Ltd (AFSL 494858). This information is of a general nature only and may not be relevant to your particular circumstances. The circumstances of each investor are different and you should seek advice from a financial planner who can consider if the strategies and products are right for you.