Benjamin Franklin – 1774.

Last financial year was a tale of two halves, the first half ending 31 December 2017 was one of a positive note as equity markets continued to trend higher based on a story of synchronised global growth, benign inflation and corporate tax cuts in the US. Unfortunately, the second half to 30 June 2018, was generally less positive. Fears that global growth had stalled and in fact reversed in some regions, the prospect of interest rates moving higher and central banks removing some liquidity together with concerns of an impending trade war all helped to keep market returns subdued.

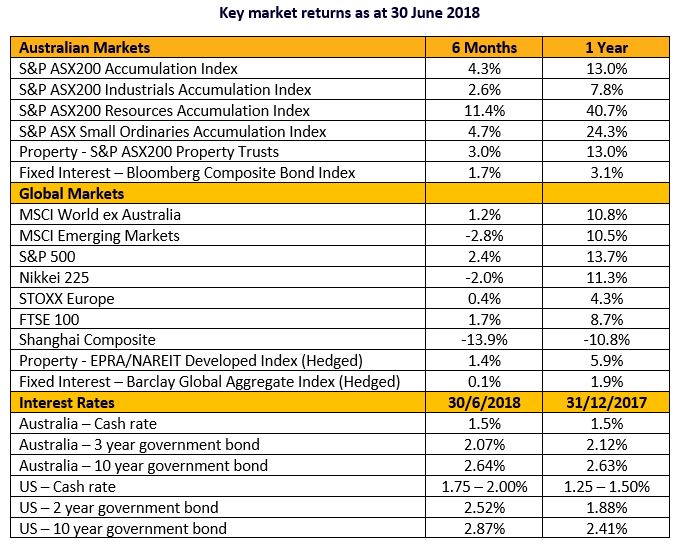

In a similar vein, the Australian equity market displayed a stark divergence of returns. Resources and energy stocks performed very strongly returning 40.7% and 38.2% respectively over the financial year thanks to soaring commodity and oil prices. The overall index return was however dragged lower thanks to the financials sector posting a loss of 3.9% on the back of slowing housing prices and the ongoing Royal Commission.

Offshore, it was a similar story with technology-based stocks such as Facebook +28.1%, Amazon +74.7%, Apple +27.7%, Netflix +161.3% and Alphabet (Google) +22.3% driving the bulk of the index returns over the financial year. These five FAANG stocks accounted for approximately 80% of the overall Nasdaq Index return of 22.3%.

The table below highlights the strength across nearly all markets over the 12 months to 30 June 2018.

Unfortunately, we think we are now heading into a period where market volatility will increase, and these sorts of returns will be harder to generate. To do so we must learn the lessons of the past but more importantly we must look to the future and try to determine what lays ahead.

When will the siren sound?

The current economic recovery is one of the longest we have seen, thanks predominantly to the massive flood of monetary easing from global central banks. With the US Federal Reserve already reducing excess liquidity and lifting interest rates and the European Central Bank announcing that it will cease pumping extra liquidity into markets by the end of this year, we think it is fair to say that we are now in the last quarter of this market cycle and the most important question we need to ask is ‘How long will it last’?

As any avid sports fan will know, the final quarter can seem to last an extraordinarily long time. Unfortunately, in the game of financial markets and economic cycles there is no set length of play for the last quarter. By looking at past cycles however, we can decipher certain attributes that help let us know the final siren is near.

As shown in the table, the synchronised global growth story helped to generate strong returns in equity markets for the financial year ended 30 June 2018. It now looks likely that we have passed the peak of this global growth though it has not yet collapsed and is still chugging along at a decent pace. Similarly, while liquidity is slowly being withdrawn, key central banks are still maintaining an easing bias. Overall, we still see reasonable growth ahead backed by central banks and to some extent accommodative government fiscal policy such as infrastructure spending and tax cuts.

Valuations

Share valuations are certainly rich in some pockets of the world however, they are far from the excessive highs we have seen in the past. In periods of low inflation and low interest rates we should expect to see valuations at slightly higher levels when compared to the long-term averages. Given the current economic conditions we remain comfortable with equity valuations and continue to favour a slightly overweight position.

Of course, there is a flip side to this story. If current valuations are justified by low rates and low inflation, what happens when either of these head higher? Again, history provides some insights. Equity markets generally continue to perform strongly until 10-year interest rates reach around 4.0%. At that point, as rates continue to climb, equity returns become more volatile and start to decline. Based upon current interest rates (refer to table) we still have some time until we reach these turning points both here and in the US. Official interest rates can move higher for a number of reasons however, the primary cause is generally inflation. If inflation starts to climb, interest rates usually follow suit.

Inflation

Over the past few years there has been a great debate raging in financial markets on whether we would ever see inflation rise again or whether it would stay low forever. Now I know, to the average person in the street this debate is as much fun as watching paint dry however, it does have ramifications for future returns and how your portfolio should be positioned. Essentially, most of the experts have taken the line that due to ageing populations, robotics, artificial intelligence and the sheer size of debt held on government balance sheets there is no catalyst for rising inflation. If inflation is a thing of the past, then interest rates will stay low for a very long period if not indefinitely.

The other camp, which we generally agree with, take the view that inflation is simply delayed. Yes, the metrics described above would keep inflation lower than historical norms but it would return. Over the last six months we have started to see signs of inflation making a comeback, hence interest rates in the US have started to head higher and the US Federal Reserve is forecasting a further two rate increases this year. Some in this camp are arguing that inflation will come roaring back primarily due to the low unemployment rate in the US. The US jobs market is at its tightest levels in some 20 years with some 6.7 million job vacancies and only 6.1 million people unemployed. Stories of staff shortages, increased wages and bonuses are becoming more common place. While it is still early days this will only escalate, pushing up prices and therefore inflation.

As we noted previously, equity markets continue to perform well while interest rates and inflation move from low to medium levels and in these periods interest rate sensitive investments tend to underperform. For these reasons we continue to favour an overweight position in equities and an underweight position in fixed interest. In short, we think the final quarter still has some time to run though the longer it does so the more we will shift portfolio holdings to cash and other defensive assets.

X-factors

At any point in time we can usually list a number of events on the horizon that could potentially be hazardous to our financial wealth. The usual suspects remain asset bubbles, political uncertainty, potential for accidental armed conflict and poor policy reforms. In most cases these tend to be nothing more than noise and while they may nudge markets in one direction or another, their lasting impact is minimal. There is however one development at the moment we are watching intensively, as the potential impact could hastily bring forward the final siren.

Trade Wars

This is the potentially escalating trade war between the US and what seems to be the rest of the world. For the most part, there is little any US President can implement and enact on their own accord as changes in law need to be enacted through the houses of parliament. Where a President can implement change is in regard to trade and the use of the military, both of which Mr Trump has been threatening to use over the course of the last six months.

Sticking to the trade aspect, Mr Trump has implemented a 25% tariff on approximately USD$36 billion of imports sourced from China. There is a further USD$14 billion awaiting sign off and last week it was announced that a further USD$200 billion of Chinese imports face the prospect of a 10% tariff. To put this into perspective the US imported approximately USD$500 billion in goods from China in 2017 so the tariffs impact roughly half of all goods imported. To date China has announced its own tariff increases matching the US dollar for dollar. The difficulty for China is that it only imported USD$130 billion in goods last year from the US. And it is not only China that is facing increased tariffs on its exports, Canada, Mexico and Europe have all been hit with increases. So far, Australia has managed to avoid a tariff increase.

“When a country (USA) is losing many billions of dollars on trade with virtually every country it does business with, trade wars are good, and easy to win,” President Trump tweeted some time ago. His thinking is that US consumers should be buying American made goods, so he should slap some tariffs on those nasty foreign exports to increase their cost and therefore Americans will buy US goods again, making America great once again.

Now I don’t want to bore you with pages of pages of economic data as to why tariffs rarely work, instead I will point out a few critical issues with this thinking and why it is very dangerous. Firstly, the US is losing billions and billions each year to other countries because Americans have a consumption led economy, not unlike our own, so they tend not to save and instead spend. The US has a trade deficit simply because they are buying goods that they no longer produce. The reason they no longer produce the items is usually because it was too expensive to do so in the USA.

To close the trade gap, Americans will either have to spend less and save more (not a great result for listed equities that rely on retail spending or the economy on the whole) or they will have to start making the goods once again on their own shores. Apart from the fact that this takes a long time (capital needs to be organised, land purchased, factories built, equipment purchased etc) as we mentioned previously, the US has the tightest labour market it has seen in twenty years. Where will the labour come from? Certainly not from Mexico and if it is not via immigration then wages will have to move higher to offer an incentive for workers to move. All in all, America can make the goods again but at what cost? Production moved offshore years ago because it was cost prohibitive; has it really changed now?

Tariffs are essentially nothing more than a tax increase. So far, the tariffs are targeted towards businesses and some retail consumption items. Mr Trump is hoping that businesses will simply absorb the cost increase on the items they import (need to run their business) and not pass it onto the consumer. Corporate profit margins are near all time highs and he just gave them a tax cut so surely they can wear that. Undoubtedly some, if not all, of the cost increase will be passed onto the end consumer sending prices and inflation higher. Higher prices will lead to demands for higher wages which leads to price increases and so the spiral starts. All the time this is happening you will have a Federal Reserve steadily increasing interest rates until we reach a point in time when corporates and consumers can no longer afford the increases and we slip into the next recession.

Keep in mind that this is not only playing out in the US in isolation. Each of the countries targeted with tariffs have and will implement their own tariffs targeting US imports. Similar factors will play out in those economies and consumers will switch from American produced goods (mainly agricultural food stocks) to other items. We have already seen Harley Davidson state it will move some of its production facilities from the US to Asia or South America so that the motorbikes that they produce will not attract the European tariffs. Perhaps these workers who will be losing their jobs can supply the labour for the new factories that will help make America great again?

Interestingly Mr Trump seems to have an ability to annoy not only US citizens, he has certainly lost friends in Germany, France and the UK with his previous comments. The reason that this is of interest is that Europe is the third largest export market for Chinese goods (the largest is the Asian region followed by America). With both Europe and China facing US tariffs, will they start to work together more closely? No doubt the Germans (who export far more than they import) will certainly be hoping so. China is the largest exporter globally followed by Europe and then the US. Any Axis between Europe and China will form an incredibly powerful exporting power house. As a trading bloc that will only increase further as China continues to switch from a production run economy to a consumption led one (it has the world’s largest middle-income demographic and the fastest growing number of billionaires).

The implementation of tariffs will not derail global growth unless it escalates much further from here. It will however slow global growth while businesses determine the impacts. It will increase costs to consumers which will see inflation picking up. All of this at a time when global growth is showing signs of a slowdown is not great, thankfully we already have low interest rates and low inflation, but the question remains – for how long?

Hopefully the escalation in the trade war is simply yet again a bargaining ploy of Mr Trump’s and therefore just the usual noise. We fear however this may not be the case and therefore remain vigilant. There is still time left in this last quarter of economic growth, but we may be nearer the final siren than we think. Only time will tell and provide yet another historical data set to be monitored in the future.

Andrew Aylward is Chief Investment Officer at Keep Wealth Partners.

Keep Wealth Partners Pty Ltd (AFSL 494858). This information is of a general nature only and may not be relevant to your particular circumstances. The circumstances of each investor are different and you should seek advice from a financial planner who can consider if the strategies and products are right for you.