Fundamentally we all understand the importance of holding some extra cash, whether it be in your wallet for that emergency purchase or in your bank account. For many of us, that sense of needing to hold onto some cash stems from the environment that we grew up in. It is really only in the last 10 years that we have seen the explosion in cashless transactions thanks in part to PayPass technology.

Therefore, with technological advancements in banking and increased settlement speeds, many people are questioning the virtue of holding cash. While this may be a fair assessment in our day to day lives, from an investment perspective cash still remains an important asset class that we all need access to.

The primary function of cash in an investment portfolio is to reduce risk. Australian residents can take advantage of the Federal Government banking guarantee that safeguards the first $250,000 of deposit holdings. This limit of $250,000 applies per person, per Authorised Deposit taking Institution (ADI) such as banks, credit unions and building societies. So, if you spread your holdings between the big four banks as an example, you can have a Federal Government Guarantee of $1 million.

The other benefit of cash in a portfolio is as a store of value. Cash is a somewhat unique investment in that it does not move up and down due to market movements or the economic conditions. Generally, $1 invested remains valued at $1 (excluding bank charges). This store of value can be very important, especially at times where you might have questions about the valuation levels of other investment assets.

If you believe investment markets are stretched, you could lock in some of your profits and hold that amount in cash while you wait for the markets to correct. Once corrected and trading at lower values you simply move your cash back into the market and wait for them to start climbing again. This sounds great and very easy, however, timing the investment markets with such clarity is extremely hard.

According to the latest data released by the Australia Taxation Office, approximately 25% of assets held in self managed superannuation funds is currently invested in cash. That equates to roughly $165 billion sitting in cash and it has been that way since the Global Financial Crisis (GFC). That is an incredible amount of money sitting on the sidelines that has not had the advantage of growing in value in line with solid returns from equity or property markets.

You pay a large price for the safety aspect of cash and that price is the significantly lower returns paid. Since the GFC, central banks globally have been pushing interest rates lower and lower and holding them at these levels in order to encourage businesses to increase capital investment via borrowings and to force excess cash holdings into more productive assets. While this has been great for borrowers it has hurt savers significantly.

Many market commentators argue that central banks have pushed interest rates well below natural levels and while there is some merit to this argument, there is another factor that has been pushing rates lower. Since the 1970’s inflation rates around the world have been falling and this has meant that interest rates have also fallen.

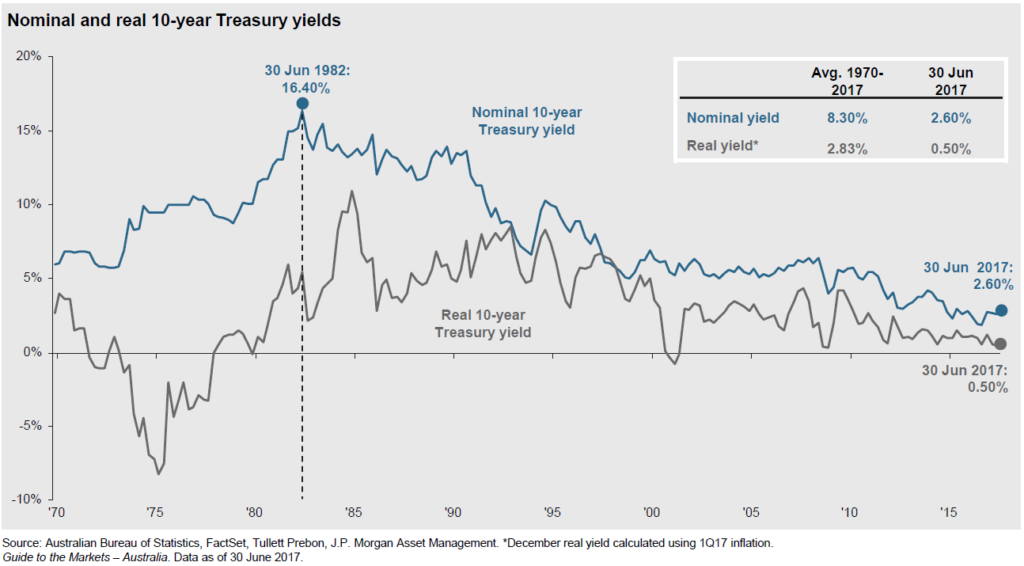

The following chart highlights the movements in the interest rate payable on the Australian government 10 year bond. The nominal rate (blue line) is simply the headline rate paid and the real yield (grey line) is that rate less inflation. Therefore, the gap between the two lines equals the inflation rate at the time.

It is clearly evident that during the 1970’s the Australian economy bore high levels of inflation and the Reserve Bank of Australia increased interest rates repeatedly during this time in order to crush the inflationary impacts. It is also evident that post June 1982, inflation decreased (the gap between the lines started to close) and so too did the overall level of interest rates. While expectations are that interest rates will start to head higher from here, we are unlikely to see the highs of June 1982 again in the foreseeable future.

The returns shown above are for government bonds and therefore do not replicate the return experience of savers who have been sitting in cash. In fact, cash returns have been significantly lower than the bond returns throughout this period to the point where most cash returns currently provide a negative real return.

This does not, however, mean that you can dispense with cash as an investment asset class. It still reduces portfolio risk and is still a stable store of value. It does, however, mean that you need to make cash work much harder in order to grind out the best possible return. Cash is often considered a lazy asset, but with interest rates so low it is imperative that it work as hard as possible.

For this reason we work with over 20 banks, credit unions and building societies in order to take full advantage of the Federal Government Guarantee and to maximise the return potential of cash and term deposits.

Keep Wealth Partners Pty Ltd (AFSL 494858). This information is of a general nature only and may not be relevant to your particular circumstances. The circumstances of each investor are different and you should seek advice from a financial planner who can consider if the strategies and products are right for you.