Investing is not an easy game. Each time you purchase a share in a company you think is great value, there’s someone on the other side of the trade who thinks it’s overvalued. As investors, we face many dilemmas on a daily basis – valuations, future prospects for companies, economic conditions, politics and regulations; the list goes on.

With so many factors at play it’s no wonder there are plenty of commentators urging caution, while others advise throwing caution to the wind. And perhaps the biggest dilemma today is whether to be more defensive or aggressive in your portfolio positioning.

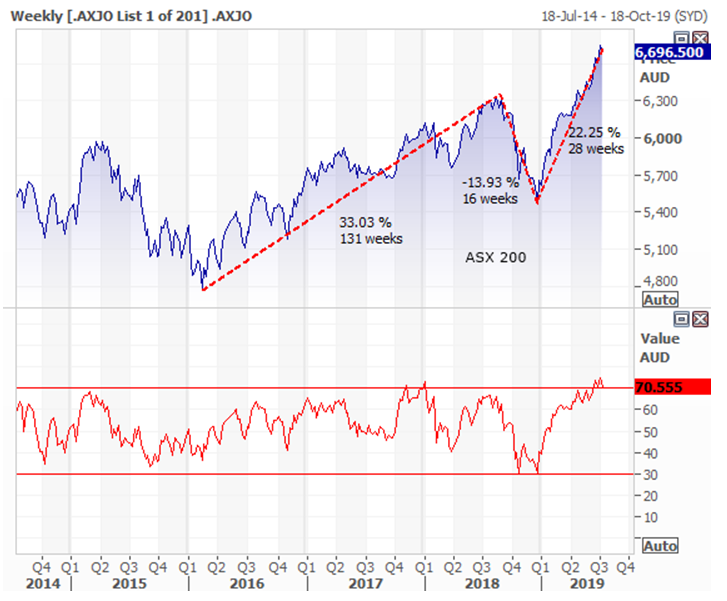

Regular readers and our clients will know we’ve preferred a more cautious approach to markets over the past twelve months. Through the second half of 2018 we felt markets were disregarding the softening global economic conditions and were underestimating the potential impact of a trade war.

When this played out keenly through December 2018, we then faced the dilemma of whether markets had overreacted the other way, especially given that any resolution of the trade war and softening rhetoric on interest rate rises could see a bounce in markets. As the chart below highlights this is exactly what occurred.

Weekly performance of the S&P ASX200 index – Source: marcustoday.com.au

The question to ask now is where to next?

Fundamentally, I don’t think that much has changed. Global growth is still slow, our housing market is still trying to find a bottom and the possibility of a trade war is still in the air. What has changed is the market psyche.

Domestically the Reserve Bank has cut the cash rate twice and may do so again towards the end of the year. At the same time the US Federal Reserve is likely to cut rates, probably next week, and the European Central Bank is also making noises that it will once again offer more support.

I admit I don’t know if this will be successful as with each stimulus the impact is diluted. It is often referred to as ‘pushing on a string’ (monetary policy works better in the other direction – pulling not pushing). I certainly hope these measures prove successful; I just worry that the markets are currently assuming that they will be. If not, shares will move lower again. But if you switch to full safety mode how do you earn a decent return with cash rates so low?

Market corrections can have a significant impact on your portfolio and your own psyche. We tend to remember large negative experiences far longer than the positive ones. So how do we quieten the noise and focus on the real return we want?

Financial freedom – what’s your number?

Focus on the overriding objective you have.

What we mean by this, is what do you fundamentally want to achieve with your life?

- Is it to retire early and never work again?

- Is it to travel the world?

- Is it to provide for your kids/grandkids?

- Is it to create a legacy for future generations?

We all have our own interpretation of what it is we’re working towards. The key is understanding how we are going to get there and maintain it. Working out the investment return required to achieve this is key to your personal financial freedom. This is your number!

Let’s assume that based on your current financial position and your version of financial freedom, if you achieve a return of say 5% per annum for the next 15 years you can start ticking off items on that bucket list you have.

Rather than focusing on what the market may or may not do every day (that’s our job) why don’t you make the 5% return hurdle your number? Better yet, make 6% your benchmark so that you build in a little bit extra.

Now that your focus is on your personal financial freedom benchmark, you don’t need to stress over what the market will do next week, next month or next year – leave that to us. You need only concern yourself about being on track to achieving your version of financial freedom.

Unfortunately, so many of us don’t know what our personal benchmark number is. That could be because we have never sat down and considered what our version of financial freedom is. It could also be the case that you have never sat down with a financial planner that truly considers your goals and helps you plan for them.

Our profession has trained itself and its clients to focus purely on the market benchmarks. We determine your risk profile and then invest your funds in a way that matches these risk parameters and tries to maximise the returns. Why does our profession do this? It wants to maximise the amount of money invested, the more invested the higher the fees.

Why don’t we flip that entire scenario around and start at what our clients want to achieve? From that point we can work out what their benchmark number is and then we can work out how their money should be invested to hit that number as a minimum. You can then decide if the risk required to get there is acceptable or, if not, how much you need to dial back on your version of financial freedom.

Surely focusing on just one number that is tailored to your vision of financial freedom is far easier. Who knows, you may even be able to start ticking off those bucket list items now rather than waiting for years and years.

If you want to find out what your number is, book in a meeting or chat with us now.

‘Being the richest man in the cemetery doesn’t matter to me… Going to bed at night saying we’ve done something wonderful, that’s what matters to me’ – Steve Jobs, co-founder of Apple.

Andrew Aylward is Chief Investment Officer at Keep Wealth Partners.

Keep Wealth Partners Pty Ltd (AFSL 494858). This information is of a general nature only and may not be relevant to your particular circumstances. The circumstances of each investor are different and you should seek advice from a financial planner who can consider if the strategies and products are right for you.