To say the events of 2020 were unexpected and full of change would be an understatement. The Covid-19 pandemic ushered in profound changes, both in markets and the way our society operates. We witnessed the steepest fall in global economic output since the Great Depression and yet the quickest rebound in markets.

Unfortunately, the toll on human life has been far more dramatic, with just over 2 million deaths and some 100 million infections at the time of writing. The dislocations to business owners, workers, families and friends have been no less severe. Undoubtedly, we all know someone who has been impacted.

And yet, we have hope that 2021 will be the year of recovery. Recovery of global economies, health and human spirit. While some countries were slower to react, all are now taking this pandemic seriously. This will aid the recovery that needs to occur.

Economies and Markets

Turning towards our economic and market thoughts, we believe that there has indeed been some structural change. The question is how long will these last?

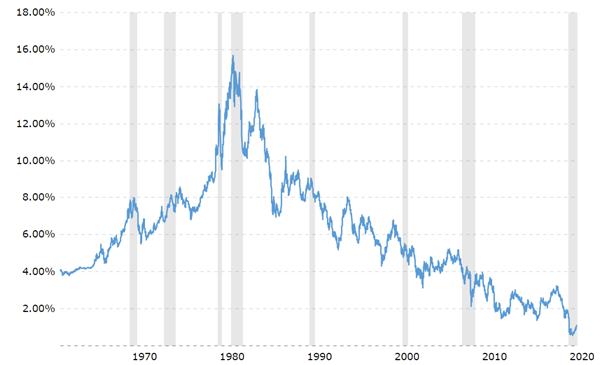

The key driver of the 2021 economic recovery will be the acceptance that interest rates will remain low for a long time. The chart below highlights the consistent trend lower in interest rates as proxied by the US 10 Year Treasury rate.

US 10-year Treasury Rate

Source: Macrotrends.net

With the economic impact the pandemic has left, there will be little desire by central banks to lift interest rates anytime soon. Central banks and governments globally have been pumping ever increasing amounts of dollars into the hands of their populations and have borrowed large amounts to finance these programs so they can ill afford to see rates increase dramatically.

Does that mean that interest rates will never increase again? The clear answer is no. Historically, the main driver of interest rates has been inflation. As inflation rose, so too did interest rates and the reverse was also true. With so much slack in the employment market both here and internationally, it is currently hard to see how we will get a steady incline in core inflation.

The other aspect is that central banks will be less concerned about reigning in inflation in the immediate future. Inflation has the benefit of debasing the amount of money needed to repay the large sums borrowed.

This doesn’t mean that interest rates will not occasionally shift higher. A sudden increase in economic output or ill-chosen words from a central banker could trigger a rise similar to the ‘Taper Tantrum’ of 2013. I believe however, that such rises will be minimal and will be short lived.

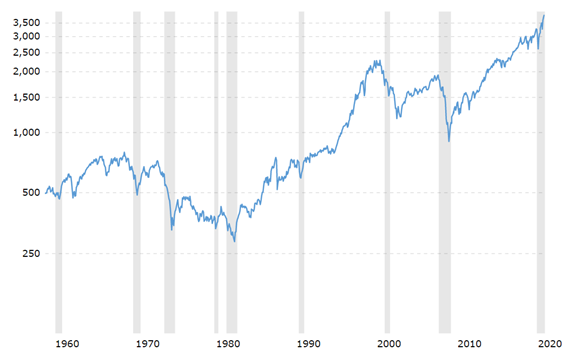

A low inflation, low interest rate environment is generally conducive to strong equity market returns and if we look at the chart below of the US S&P 500 Index you will notice that it is almost the opposite of the US 10 Year Treasury Rate that I highlighted earlier.

US S&P 500 Index

Source: Macrotrends.net

Some of you will look at these charts and ask if we should just put everything into equities and forget about fixed interest and defensive assets?

You certainly still need to hold onto some defensive assets; shocks don’t just occur in our lives, they also occur in markets. In those times of market upheavals, and there will be more to come, you need to be holding some defensive assets in your portfolio.

While holding defensive assets is still very prudent, we need to acknowledge that the returns on offer will be lower by historical standards. With this in mind, I believe that portfolios will need to hold larger allocations of growth assets in the years ahead. This, however, will come with higher volatility.

I fully expect that our economies will rebound on the economic side in 2021. This will be helped in large part by the rollout of the numerous vaccines, yet that will not be the only catalyst. The pandemic has generated far greater change; it has changed the political order. China’s aggressive assertions that it was not the source of the pandemic has to some extent ostracised its markets and capital. Cheque book diplomacy is now viewed in a different light.

We have also witnessed the demise of a president and a shift in power in the United States. With control of both houses of parliament under one party, government policies have swiftly changed and there will be greater focus on the inequalities that abound in society. There will also be much greater focus placed on sustainability and infrastructure in the years ahead.

Supply chains of multinationals have been shocked into change, the focus is no longer simply on the cheapest price but now on resilience and reliability. This will favour more of the emerging market countries as well as some domestic corporates as the source of our products expands.

The other critical change has been in how we work and gather information. New industries have been born overnight and the pandemic has sped the technological take up. Many tech industry experts have suggested that we have seen 5 to 10 years’ worth of advancement and take up in the last twelve months. The impact derived from these changes will be far reaching and not yet fully understood. Take for example the upsurge in rural property prices; will this be sustained due to the shift in how and where we work?

Life is mostly froth and bubble1

Perhaps a far greater question that some will be asking is are we just fuelling yet another bubble that will eventually burst? I think the best way to answer that is to say, in the short term – no, but in the long term, probably. There are certainly some sectors where asset prices have risen dramatically and are well ahead of traditional fundamentals. Some share prices are currently factoring in many years of rapid growth and we will have to wait and see if such companies can grow into those prices.

With the current outlook for interest rates and inflation, I think that barring a critical failure of the vaccination programs, it will take some years for the conditions of a bubble to take hold fully. We do however need to be cognisant that central banks and governments are building the conditions that do allow bubbles and therefore we need to remain vigilant.

Finally, it is the dislocations of 2020 that once again remind us of the need for a solid financial plan. Life is nonlinear, there are always things that come at us out of the blue, that is both the joy and the pain of being human. Just as our life changes, we need our plans to change but we also crave the familiarity and that is where a good financial adviser, who is with you for the long haul, can help.

If 2020 has shown us nothing else, it has proven that we are resilient, that there are those among us who will stand tall in times of challenge and adversity and that we should take the time to reach out to our families and friends to check in on them.

May 2021 be a year of recovery for all of us.

1. Adam Lindsay Gordon – 19th century Australian poet (a statue on Spring Street commemorates him, for those interested).

Andrew Aylward is Chief Investment Officer at Keep Wealth Partners.

Keep Wealth Partners Pty Ltd (AFSL 494858). This information is of a general nature only and may not be relevant to your particular circumstances. The circumstances of each investor are different, and you should seek advice from a financial planner who can consider if the strategies and products are right for you.