“May you live in interesting times”. We do, and what a year it’s been.

We witnessed the (“best ever attended”) inauguration of Donald ‘Tweet’ Trump, and then some 420 protest marches in the US and in a further 168 countries decrying his election. The United Kingdom formally triggered Brexit. We’ve witnessed escalating political tensions around China, North Korea and the Arabian Peninsula and our own political debacle about who can sit in parliament representing a nation where it is estimated that up to 50% of the population are ineligible for election due to either their parents or themselves being born overseas.

Interestingly though, investment markets simply shrugged off the news, remained calm and kept climbing as witnessed by the returns to 30 November 2017 below:

Thanks to the improved economic environment, equity markets have continued to climb, with US indices marking new highs over 60 times in 2017. Synchronised global growth, positive corporate earnings and low interest rates suggests the path of least resistance for markets is still higher.

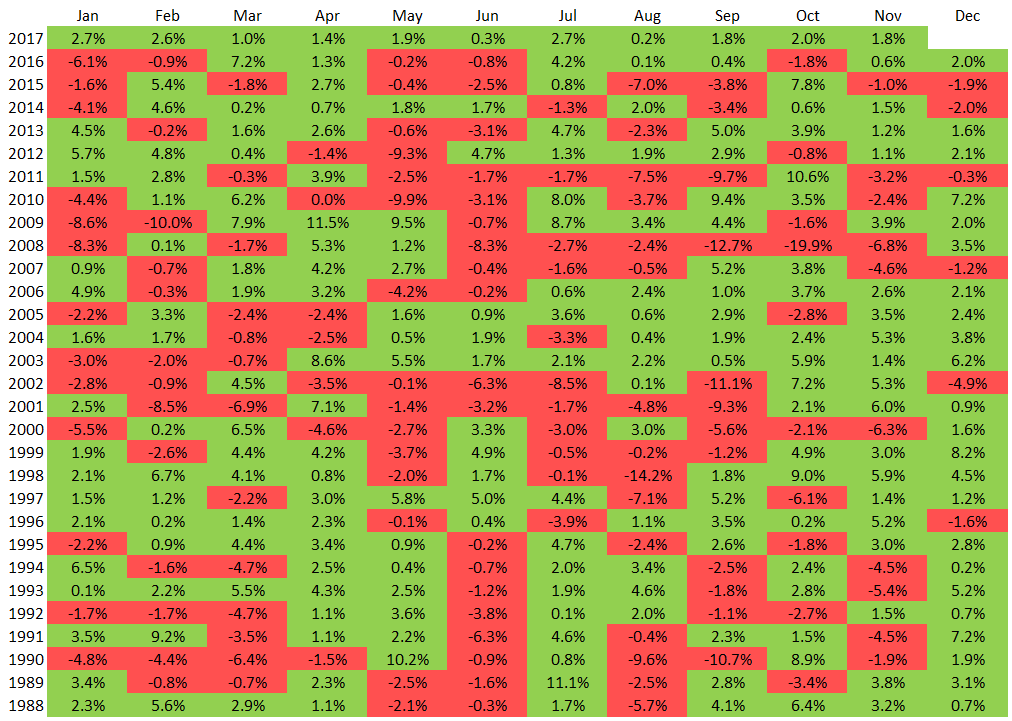

The table below, courtesy of Charles Schwab, shows the monthly change in the MSCI AC World Index since inception in 1988. What should stand out almost immediately is the fact that this global index has risen for 13 months straight, the longest stretch since 2003/2004.The other interesting point is that the 2017 calendar year is yet to see a negative month, something that has never previously occurred.

There is an old market saying “Bull markets do not die of old age, they are killed by excess or central banks”. Such a saying is very timely at the moment as the US equity markets close in on their longest recovery period and therefore it is very easy to say that it must surely end. End it will, but there needs to be a catalyst and at the moment it is hard to see where that catalyst will emerge from.

As the U.S. Federal Reserve embarks on a five to six-year monetary policy tightening journey to normalise its balance sheet and interest rates, the U.S government is also on the brink of major tax reform which could add in excess of US$1.4 trillion to the deficit in addition to a promised US$1 trillion boost to infrastructure spending over 10 years. As GDP growth accelerates, fiscal policy should be moderating, not expanding. This clash will potentially make the task of the new Chairman of the U.S. Federal Reserve Jerome Powell and the Federal Open Market Committee (FOMC) more challenging.

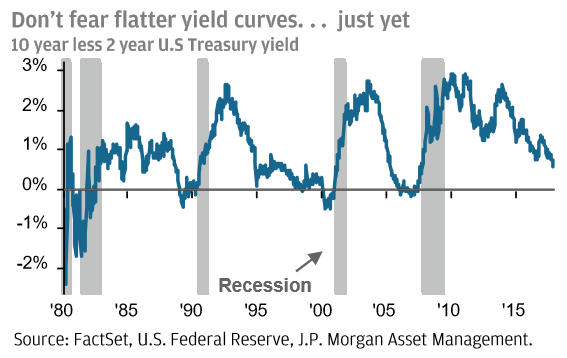

The following chart from J.P. Morgan Asset Management shows that the last five US recessions have occurred on average five months after the bond curve inverts, that is when two year interest rates are higher than 10-year interest rates. The good sign is that whilst the curve has flattened it is not yet at this trigger point.

Supporting this observation that markets have further to move is that equity markets are at best fairly-valued and at worst slightly stretched. Obviously, we need to consider each individual market as to the valuation attractiveness. At the moment we still favour the European and Japanese markets from an international perspective and remain neutral to underweight on the US market.

In regards to the Australian economy, there are two distinct camps. Those who are pessimistic on growth and believe that the housing market is headed for a significant downturn, wages remain soft and therefore consumer spending low. The other side see glimmers of strength emerging with a rebound in commodity prices, increased infrastructure spending and only a modest slowdown in housing. A continual tightening in the labour market will also eventually lead to wages growth.

We tend to favour the second argument and point to the increase in the population as one of the contributing factors. Australia’s population is rising at 1.6% p.a. and is expected to hit 25 million people in 2018. While this does not sound that impressive it is roughly the equivalent of adding two Hobarts each year. Victoria is currently taking the lion’s share of the population growth and is growing at 2.3% p.a. or approximately 3,000 people per week. The most pleasing part of the growth is that the majority is from overseas migration which is putting a tailwind behind the housing demand and infrastructure needs that are to be built over the coming decade.

In short, we remain watchful of investment markets but firmly believe there is still further expansion available. That being said, the tailwinds of the last five years, low volatility and low interest rates, are starting to turn and are becoming headwinds.

Looking ahead

As mentioned earlier, bull markets are killed off by excess or central banks. The magnitude and cause of a market correction is difficult to predict and investors are currently oblivious to an exogenous factor, but there is abundant fertile ground in which one can sprout.

At present, the most likely catalysts for a correction are political fallout relating to President Trump being impeached, conflict drawing in the US in the South China Sea, North Korea and the Middle East or lastly, a dramatic lift in interest rates.

Impeachment of President Trump seems somewhat remote at the moment, though the probe into Russia’s involvement in the 2016 election continues. Conflict at this stage also seems improbable, though with the Donald and Kim Jong-Un trading schoolyard insults North Korea remains the most likely trigger point. Interest rates seem to be the most likely catalyst but this would require a spike in inflation which remains stubbornly low.

Inflation has been restrained by factors such as globalisation, technological advancements (robotics, artificial intelligence and connectivity speeds) and competitive developments (Uber and Amazon for example). Historically, low unemployment levels have led to increased wages, however these productivity developments have created an environment where wage growth has been sluggish at best averaging just under 2% globally.

The US Federal Reserve expects inflation to gradually rise over the course of 2018 & 2019 and is forecasting three rate increases next year and expects the cash rate to be near 3.0%. The key risk to markets at present is that the market is only factoring in 1.5 rate increases or a cash rate nearer 2.0% than 3.0%.

In the past two US rate hike cycles, in the 1990s and the 2000s, inflation did overshoot, which compelled the Fed to push the policy rate (well) above neutral. Current “Goldilocks” markets discount this possibility.

If inflation does start to spike higher than expected we are likely to see the US Fed increase rates and the pace of its quantitative tightening. The European Central Bank is also likely to stop its easing program and start restoring the cash rate to a neutral level. All of this would lead to a reduction in liquidity and a reassessment of the current valuation levels of equities. Keep in mind that central banks have pumped in excess of US$15 trillion into markets in the last 10 years. This is an unprecedented amount and at some point the bulk of it needs to be removed.

The Reserve Bank of Australia is unlikely to move interest rates in 2018 unless we see a dramatic increase in wage growth; our economy is simply too sluggish at the moment and any increase in US rates should lift the US dollar and therefore suppress our dollar. Due to expected US interest rate moves we see the Australian dollar being softer for the first half of 2018 and only picking up again towards the end of the year. If US interest rates do increase, Australian bank funding costs are likely to increase as well, which could see the banks move independently of the RBA.

Australian equities have lagged their international counterparts but this also means that they are not as richly priced and therefore may temper the amount they contract should a correction occur. Corporate bonds have also performed exceptionally well thanks to the demand for higher yields. Interestingly it is the riskier bonds (those paying higher yields) that have outperformed. In an environment of rising interest rates we prefer to hold higher quality bonds that provide greater safety. As US interest rates rise, offshore investors will start to switch some of their AUD holdings back to USD holdings and this could see lower quality bond prices fall.

Lastly, the Chinese government is trying to rebalance its economy from the ‘old’ to the ‘new’. It is achieving this by restricting lending to the old economy sectors and allowing defaults whilst providing support and ample access to lending for the new economy sectors. Any old economy defaults will not create a systematic risk to the broader economy.

Growth is likely to remain around 6% over the next couple of years, however there is likely to be less demand for Australia’s hard commodities and more of a focus on services we can provide and soft commodities such as food and consumer consumption goods. In order to keep riding the Chinese dragon, Australian businesses must pivot to these new consumption trends.

I for one hope that the investment party will continue for many years to come, but with valuations becoming stretched in some markets it is good to remind yourself that hope and luck are the partner of a gambler and not an investor.

Keep Wealth Partners Pty Ltd (AFSL 494858). This information is of a general nature only and may not be relevant to your particular circumstances. The circumstances of each investor are different and you should seek advice from a financial planner who can consider if the strategies and products are right for you.